МАНИПУЛЯЦИИ РЫНКОМ ЦЕННЫХ БУМАГ С ИСПОЛЬЗОВАНИЕМ ЗАКРЫТЫХ ИНФОРМАЦИОННЫХ КАНАЛОВ

Aннотация

Развитие социальных сетей и платформ мгновенного обмена сообщениями изменило способ распространения финансовой информации, упростив доступ к ней, но в то же время предоставив возможности для потенциальных злоупотреблений. Среди этих платформ Telegram приобрел значительную популярность в русскоязычном сегменте, особенно благодаря своим каналам с инвестиционными рекомендациями. Эти закрытые каналы, часто требующие платы за предоставление доступа, привлекли множество частных инвесторов, стремящихся извлечь выгоду из якобы экспертных прогнозов. Однако это явление также представляет собой значительный риск манипулирования рынком, особенно в отношении низколиквидных акций. Механизм манипуляции, требующий наличия некоторого количества частных инвесторов, предполагает привлечение их интереса к биржевым активам с дальнейшим повышением стоимости ввиду возросшего спроса. Манипулятор использует выросшую стоимость актива для закрытия позиции и фиксации прибыли.

В данной статье рассматриваются подробные механизмы таких манипуляций и предлагаются методы борьбы с ними.

К сожалению, текст статьи доступен только на Английском

Introduction

Mechanisms known as "pump and dump", which attract the attention of investors by various means, including conventional advertising, have been around for a long time. Studies on the influence of such advertising on stock prices [Frieder, L and Zittrain, J., 2007] have shown that the period of active launch of an advertising campaign is preceded by a day with almost guaranteed positive returns. Based on the data obtained, it can be assumed that purchases of the securities to be promoted by the advertisement are made during these days. When the market stabilises after the "acceleration" of the quotations, there is a fall in the price, as a result of which investors who bought securities during the advertising campaign receive a negative return of 5.5% on average.

Mechanisms of promoting securities through information channels are also used by portfolio managers who need to close a large position without losses from the volume effect [Hong, H. and Huang, M., 2002]. Increased demand for a security allows the manager to "close" the position promptly to retail investors by placing limit orders to sell. Similar manipulations can be used when it is necessary to open a large position without moving the price significantly above the current one.

In the case of e-mail spamming, the mechanism is comparable to that of advertising campaigns [Böhme, R. and Holz, T., 2006]. Characteristic features of the bidding behaviour are an increase in trading activity in the stocks mentioned in the mailings and positive abnormal returns shortly after the mailings.

The existing studies describe the mechanism of "pump and dump" using information contained in open sources (advertisements, e-mail distribution). Mechanisms to combat such manipulation schemes are mainly limited to increasing the level of investor education. However, there are mechanisms where the psychological impact on investors is much more significant than when they use information from open sources. Such mechanisms use closed information channels to which access is provided for a fee.

Purpose of the paper: to describe the mechanism of the impact of the "insularity" of alleged insider information on investors' incentives to buy shares in the "pump and dump" mechanism.

Materials and research methods

Firstly, the mechanism of the "pump and dump" scheme, as it operates on the social network Telegram, will be described in greater detail. Secondly, the consequences of the spread of such schemes will be described, and the peculiarity of the influence of "closed" information in the publication of recommendations to buy assets will be determined. Thirdly, some proposals will be presented on methods to combat speculation by information flows on the stock market.

The results of the study and their discussion

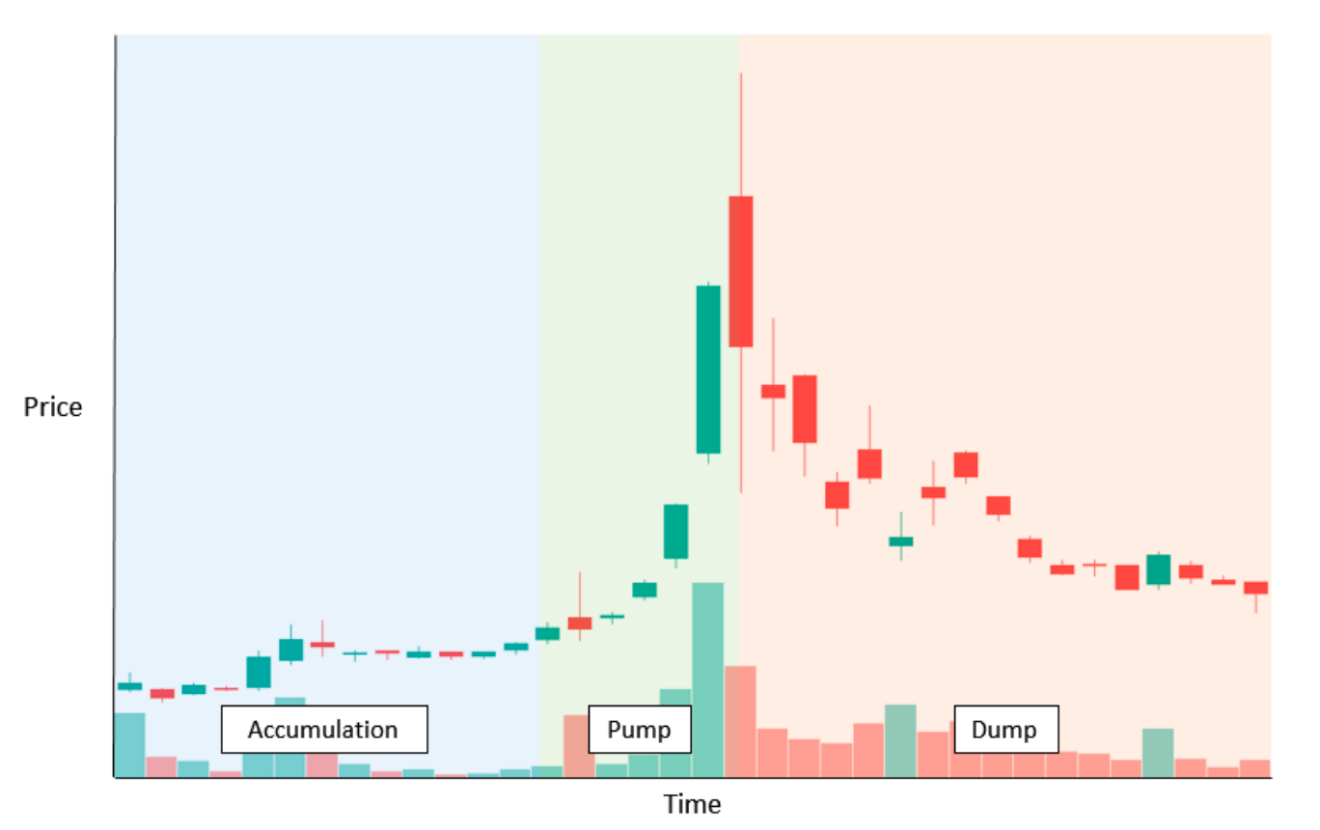

The mechanism of manipulation

Prior to initiating the manipulation, it is essential to secure an investor for the closed channel. Audiences are drawn to advertising in channels with analogous subject matter, as well as channels offering complimentary access to select predictions from the paid channel. The invitation encompasses:

- The anticipated return on investment for the investor participating in the trades recommended by the channel.

- A description of the strategy is provided, including a delineation of the assets utilized in the investment, the strategic objective, and, in some cases, the investment horizon and potential risks.

- The financial outlay required to gain access to the closed channel.

The following section will provide an overview of the "pump and dump" mechanism.

- The acquisition of an asset.

The manipulation process commences when the creator of the Telegram investment channel identifies and acquires a substantial position in the asset that they intend to manipulate. The most pronounced manipulation effect can be achieved with third-tier stocks, as they are low-liquidity stocks and any anomalous change in supply or demand for such securities has a considerable impact on their price [Liu, P., Smith, S.D. and Syed, A.A., 1990]. This feature is employed to augment the effect of subsequent manipulative actions [Pradhuman, S.D., 2000].

- The formation and distribution of false forecasts

Once a position in a stock has been obtained, the channel creator produces a detailed and ostensibly authoritative forecast. This forecast must appear credible and frequently includes:

- numerical figures, such as specific financial figures such as projected earnings, revenue growth, or margins;

- optimistic forecast regarding the company's future prospects, strategic initiatives, or upcoming product launches.

- comparison with similar companies with the objective of identifying undervaluation or significant growth potential.

Subsequently, these forecasts are disseminated via a private Telegram channel. Subscribers who have paid for access to this channel believe that they are receiving exclusive, insider information.

- Investor Reaction and Market Impact

Subscribers implement the recommendations promptly, as they believe in the validity of the forecast. The collective buying power of numerous private investors creates a sudden surge in demand for low-liquidity stocks, which raises their price dramatically.

- Profit generation by the channel creator

As stock prices increase due to artificially induced demand, the channel creator, capitalising on the price rise, sells previously purchased shares, thereby generating a substantial profit. Once the channel creator sells his position, the artificially inflated demand dissipates, frequently resulting in a precipitous decline in the stock price [Nam, D. and Skillicorn, D.B., 2023]. Late and less informed investors who purchased shares at higher prices sustain losses [Siering, M., 2018].

Fig. Pump and dump manipulation scheme

A number of distinguishing characteristics can be identified in these manipulative practices.

- Transactions are based on recommendations from closed, paid Telegram channels, which creates the impression of exclusive access to valuable information [Judge, P., Alperovich, D. and Yang, W., 2005].

- Investors are required to pay a fee to participate in these channels, which creates the perception of gaining insider knowledge or a competitive advantage.

- Channels frequently provide consensus forecasts for highly liquid assets with the objective of establishing trust, while individual forecasts target low-liquid assets that are more susceptible to manipulation [Nelson, K.K., Price, R.A. and Rountree, B.R., 2013].

- A series of initially successful trades serves to reinforce the credibility and trustworthiness of the forecasts, thereby encouraging further investor participation.

The impact of information insularity on investor actions

The perception of receiving exclusive insider information significantly influences investor behaviour. When private investors believe they are gaining access to secret, privileged information, their actions are determined by a number of psychological and financial factors.

- An enhanced perception of value.

Investors frequently ascribe greater value to information that is perceived as exclusive or limited in availability. This bias causes them to favour and act on such information more readily than on publicly available data. Additionally, investors may exhibit confirmation bias, interpreting exclusive information in a manner that is consistent with their pre-existing beliefs or desires for profitable investments.

- Increased credibility and trustworthiness.

Exclusive outlets frequently present their forecasts in a manner that conveys an aura of authority and expertise, which increases investor confidence. Investors may believe that paying for access to information correlates with its higher quality and reliability. The first successful trades based on such forecasts build trust and credibility, leading to repeated and increased use of exclusive information.

- Accelerated decision-making.

The exclusivity of information engenders a sense of urgency. Investors are fearful of missing out on profitable opportunities, which encourages them to make decisions and act promptly. The perceived insider nature of information can cause investors to bypass scrutiny, relying solely on the advice provided.

- Collective behaviour and herd behaviour.

Investors within these exclusive channels frequently observe and emulate the actions of other group members, thereby reinforcing the collective influence on the share price. This herd behaviour can result in significant market movements, particularly in low-liquidity stocks. The positive feedback generated by the initial profits generated by the group's actions serves to reinforce the belief in the accuracy of the information, thereby supporting the collective buying or selling cycle.

- Overconfidence and risk-taking.

The conviction that one possesses privileged information may engender the impression of control over market outcomes, prompting investors to undertake greater risks, execute larger trades, and utilise greater leverage. The belief in the exceptional worth of exclusive information may prompt investors to concentrate their portfolios on recommended assets, thereby neglecting diversification and heightening exposure to market manipulation risks.

- A possibility of substantial financial losses.

In instances where information is employed as a means of manipulation, the initial artificial price rise is often accompanied by a surge in investor interest. However, subsequent to the sale of positions by the manipulators, the stock price frequently declines, resulting in substantial losses for those who have acquired the stock at a later stage. The abrupt realisation of the manipulation and the subsequent losses can give rise to emotional distress, panic selling and a loss of confidence in future investment opportunities.

Legal and ethical implications of the aforementioned methods.

The aforementioned methods constitute forms of market manipulation that are both illegal and unethical for a number of reasons. The recommendations are not based on genuine financial analyses; rather, they are designed to generate artificial demand and inflate stock prices. Furthermore, private investors are misled into entering into transactions that primarily benefit the creators of the channel, to the detriment of the investors. These manipulative practices distort the natural price discovery mechanism of the stock market, thereby undermining its integrity and efficiency.

Measures to combat market manipulation.

The most effective method of combating manipulative practices is a multi-pronged approach that engages the participation of regulators, platforms, and investors.

- It is recommended that regulators enhance their monitoring of social media and messaging platforms with a view to identifying any suspicious activity related to stock recommendations. This may be achieved by utilising advanced analytics and artificial intelligence to discern patterns that are indicative of manipulation.

- The legislative framework should be reinforced with the specific intention of addressing and penalising manipulative activity. This should include the imposition of rigorous sanctions and the filing of lawsuits against individuals and entities involved in market manipulation.

- Regulators should collaborate with messaging platforms, such as Telegram, to guarantee that they have established procedures to monitor and report suspicious activities related to financial advice and share trading [Siering, M., Clapham, B., Engel, O. and Gomber, P., 2017].

- It is imperative that comprehensive information campaigns be implemented to educate investors about the inherent risks associated with receiving investment advice through unregulated channels. These campaigns must emphasise the potential dangers of manipulation and the vital importance of due diligence.

- The necessity of conducting independent research and seeking counsel from duly licensed financial advisers in lieu of relying on unverified sources should be elucidated.

- It is necessary to educate investors on how to verify the credibility of sources providing financial forecasts and advice.

- The implementation of systems to verify individuals and entities providing financial advice on the platform is required. Vetted advisers must meet certain criteria and adhere to ethical standards.

- It is necessary to implement user-friendly reporting mechanisms that allow individuals to flag any suspicious activity or recommendations that appear manipulative [Zahedi, F.M., Abbasi, A. and Chen, Y., 2015].

- The utilisation of artificial intelligence and machine learning to monitor and moderate content related to financial advice, thereby ensuring compliance with regulatory requirements and ethical standards, can also assist in combating manipulative practices.

Conclusion

The perception of receiving exclusive insider information has a profound impact on investor behaviour, often leading to quick decision-making, overconfidence and exposure to market manipulation. In order to protect investors from the negative effects of manipulative practices, it is essential to understand the psychological and financial implications of such practices and to combine the efforts of regulators, educational initiatives and platform policies. It is therefore necessary to raise awareness and vigilance in order to preserve market integrity.

Список литературы