РАЗВИТИЕ ЦИФРОВЫХ ФИНАНСОВЫХ АКТИВОВ В УСЛОВИЯХ ТРАНСФОРМАЦИИ ФИНАНСОВОГО РЫНКА

Aннотация

В данной статье рассматриваются технологические характеристики цифровых финансовых активов (ЦФА), а также их значение для развития современных финансовых рынков и цифровизации финансовой системы России. Анализируются специфика выпуска и обращения цифровых финансовых активов, а также роль Банка России и операторов информационных систем в функционировании рынка. Особое внимание уделяется разграничению ЦФА, криптовалют, стейблкоинов, цифровых валют центральных банков и гибридных цифровых прав, сочетающих в себе свойства цифровых финансовых и утилитарных цифровых инструментов.

В исследовании анализируется текущее состояние и ключевые тенденции развития российского рынка ЦФА. Рассматриваются взаимодействия между его ключевыми участниками, включая эмитентов, инвесторов, операторов бирж, номинальных держателей и регулирующие органы. Также исследуются новые типы токенизированных инструментов, включая ЦФА, связанные с криптовалютами, товарами и отдельными макроэкономическими показателями.

Авторы отмечают, что цифровые финансовые активы предлагают ряд преимуществ как для эмитентов, так и для инвесторов. К ним относятся упрощение процедур выпуска, снижение транзакционных издержек, повышение операционной прозрачности, расширение доступа к альтернативным инвестиционным инструментам и снижение барьеров для входа участников рынка. Однако также отмечаются существующие проблемы развития этого сегмента, включая низкую ликвидность вторичного рынка, недостаточную интеграцию информационных систем, сложности регулирования гибридных цифровых инструментов и ограниченное раскрытие информации об эмитентах.

В заключение делается вывод о том, что рынок цифровых финансовых активов имеет значительный потенциал для дальнейшего развития и может стать важным инструментом для инвестиционной деятельности, токенизации активов и международных расчетов. Дальнейшее расширение рынка будет в значительной степени зависеть от улучшения нормативно-правовой базы, развития инфраструктуры, налогового регулирования и внедрения более сложных цифровых финансовых продуктов.

Ключевые слова: токенизация, блокчейн, смарт-контракты, цифровые валюты центральных банков, криптовалюты, цифровые финансовые активы

К сожалению, текст статьи доступен только на Английском

Introduction

The development of blockchain technologies and decentralized finance has become one of the key trends shaping the transformation of the global financial system. Distributed ledger technologies are increasingly being integrated into financial markets, creating new approaches to asset circulation, investment processes, and digital interaction between market participants. In this context, digital financial assets (DFAs) have emerged as a new financial instrument combining elements of traditional finance with the technological capabilities of blockchain infrastructure. The growing interest in DFAs is driven by their potential to increase transaction speed, improve transparency, reduce operational costs, and expand access to alternative investment instruments.

At the same time, the digital financial assets market remains at an early stage of development and continues to undergo institutional and infrastructural transformation. The formation of this segment is accompanied by the emergence of new financial products, changes in market architecture, and the search for effective mechanisms of interaction between issuers, investors, and platform operators. Under these conditions, the study of the current state of the DFA market, its structural characteristics, development trends, and existing limitations becomes particularly relevant in the context of the ongoing digitalization of the financial sector.

Blockchain systems in the context of development of decentralized finance have been in the focus of economists around the world in recent years, in particular issues related to the use of distributed registry technologies in finance have been studied by authors such as Li et al. (2015), Tian et al. (2020), Kudryashova et al. (2021), Aleshina et al. (2022), Chen et al. (2022), Abuzov A.Y. (2023), Chen et al. (2024), Zhang et al. (2024).

Akulinkin (2023) has written about the use of blockchain in the formation of cross-border payment infrastructure.

The issues of classification of various crypto-assets have been investigated by Kochergin (2022), Osmolovets (2022), Korneluk (2024).

The functioning of digital currencies of central banks is the subject of studies by such scientists as Cao H. et al. (2023), Gorbacheva T.A. (2024).

The specifics of introduction into the Russian market and operation of digital financial assets (DFA) as an analogue of tokenized assets have been considered by Ageyev et al. (2020), Mitrofanov et al. (2024), Pertseva (2024), Stankevich et al. (2024). In particular, Mnatsakanyan et. al (2023) have written about the identification of risks of investments in digital financial assets. In the context of international financial settlements, the possibilities of using DFAs were considered by Vasilevsky (2024).

The analogue of tokenised assets on the Russian market is a new investment instrument called digital financial assets (DFAs). The issue and circulation of DFAs is state-regulated.

Digital financial assets include digital rights that may include:

1. Monetary claims.

2. The ability to exercise rights under securities.

3. The right to participate in the capital of a non-public joint-stock company.

4. The right to demand the transfer of securities [Federal Law No. 259-FZ of July 31, 2020].

Digital financial assets are built on blockchain technology, where all transactions and operations are recorded in a distributed ledger. This technological framework enables market participants to interact directly through smart contracts within the blockchain network, reducing the need for intermediaries and supporting a decentralized transaction environment.

Blockchain itself represents a distributed database that stores information about all transactions conducted by participants of the system. Data are organized into interconnected blocks, each containing a set of verified transactions. One of the key features of blockchain technology is the immutability

of stored information, which enhances the transparency and reliability of operations performed within the network.

A smart contract may be defined as a digital agreement created within a blockchain environment. Unlike traditional electronic contracts, smart contracts are capable of automatically executing predefined conditions, including the transfer of funds or other digital rights, without requiring additional manual intervention.

In this regard, digital financial assets can be viewed as digital representations of traditional financial instruments, including shares, bonds, bills, loans, and other assets. They function as digital rights or tokenized certificates with a specific value, operating within blockchain-based or other decentralized information systems. There are also hybrid digital assets that simultaneously include DFAs and other digital rights, such as the right to demand the performance of work or the provision of services, the right to use goods or discounts. In other words, hybrid digital assets have the characteristics of both DFAs and utilitarian digital rights (UDRs).

Hybrid digital rights (HDRs) represent a form of digital contract that allows investors to choose the form of settlement, including cash payments, property rights, or goods. In this respect, HDRs differ from traditional digital financial assets, which provide for the exclusively monetary form of fulfillment of obligations. Although HDRs can be considered a variety of DFAs, they provide broader opportunities for investors, including the right to demand the transfer of goods, services, completed work, or exclusive intellectual property rights. Thus, HDRs combine the characteristics of digital financial assets with elements of utilitarian digital rights (UDRs).

Almost the entire hybrid digital financial assets market is represented by issues on art objects. Such issues are simultaneously digital financial assets and utilitarian digital rights that allow the transfer of a right to use part of an audio-visual work (films, commercials, reports, etc.). These issues do not provide for the transfer of real art objects.

Although digital financial assets (DFAs) and hybrid digital rights (HDRs) are both based on distributed ledger technology and smart contracts, they should be distinguished from other types of digital instruments. Despite certain external similarities, these instruments differ significantly in their legal status, operational principles, and economic functions.

Firstly, a DFA is, in fact, a digital record in a blockchain system certifying the rights to claim a particular asset, whether it be cash, stocks, bonds, precious metals, oil, real estate or something else. DFAs and cryptocurrencies use the same technology (blockchain), but cryptocurrencies, such as Bitcoin or Ethereum, unlike DFAs, are not considered a type of digital rights under which the issuer has obligations to investors. Another difference from cryptocurrency is the infrastructure. DFAs can only circulate within their information systems, whereas cryptocurrencies can be handled on all blockchains with which they are technically compatible.

Secondly, stablecoins are a type of cryptocurrency tied to real assets, such as currencies of different countries, natural resources, real estate (e.g., USTD, issued by Tether Limited). Stablecoins have lower volatility compared to cryptocurrencies and are mainly used by traders to move assets between exchanges, but they are also gradually taking root in the consumer payments sector [RBK, 2024]. Unlike stablecoins, DFAs are issued by issuers that have passed a financial reliability check and have legal obligations to investors. The emission itself is organized by platforms registered by the regulator, the Central Bank, in a special register.

Thirdly, DFAs should be distinguished from central bank digital currencies (CBDCs). CBDCs are digital currencies issued by the central banks of countries. The value of cryptocurrencies depends on many factors, including the balance between supply and demand, while the value of CBDCs is determined by the central bank and is equal to the country’s fiat currency (e.g., the Sand Dollar is a digital analogue of the Bahamian dollar, or the Jam-Dex is a digital Jamaican dollar). CBDCs perform all the functions of money as a means of payment, a measure of value, and a store of value on par with cash and non-cash forms of country’s currency. Transactions in CBDCs are not anonymous, which allows the state to combat the shadow economy and tax evasion. Many countries are in the testing phase of CBDCs (Digital Ruble in Russia, e-CNY in China, e-Rupee in India, etc.). Furthermore, the Eastern Caribbean Central Bank, which unites eight Caribbean countries (Antigua and Barbuda, Grenada, Dominica, Saint Vincent and the Grenadines, Saint Kitts and Nevis, Saint Lucia, Anguilla, and Montserrat), launched a pilot version of the digital currency DCash in 2021. This is the first retail CBDC that also operates cross-border, effectively uniting several island nations into a single digital financial system [TASS, 2023]. Unlike central bank digital currencies, DFAs are not used to pay for goods and services.

The technical characteristics of Russian digital financial assets also differ from those of the real-world asset (RWA) tokenisation models commonly used in the global cryptocurrency market. In Russia, DFAs may be issued only through information system operators included in the official register of the Central Bank. Accordingly, a token issued outside this regulatory framework or without an officially approved issuance decision cannot be recognized as a DFA. By contrast, RWA tokens in the global crypto market can generally be created and circulated by virtually any market participant without comparable regulatory restrictions.

Main part

The legal framework for digital financial assets (DFAs) is founded upon two federal laws and a number of regulations issued by the Bank of Russia. Federal Law No. 259-FZ of July 31, 2020, “On Digital Financial Assets, Digital Currency, and Amendments to Certain Legislative Acts of the Russian Federation” is the primary document defining the concept of DFAs and the procedure for their issuance and circulation. Federal Law No. 259-FZ of August 2, 2019, “On Attracting Investments Using Investment Platforms” regulates crowdfunding and token issuance. Bank of Russia regulations establish requirements for DFA exchange operators, information security, and investor protection.

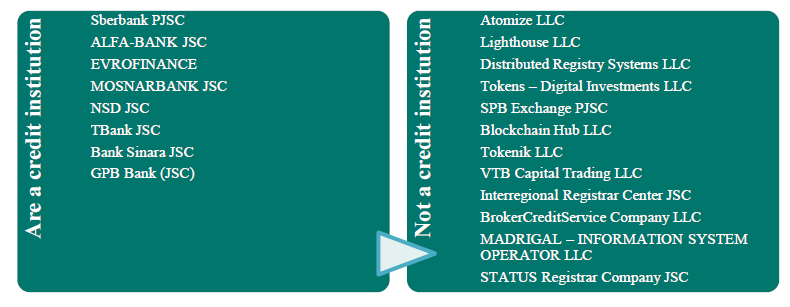

In Russia, information system operators (ISO) are responsible for issuing DFAs. The ISO status allows for the issue and accounting of DFAs. Information system operators can only be Russian legal entities included in a special register, which are closely supervised by the Bank of Russia. According to this register, there are currently 18 ISOs operating on the Russian market (Figure 1).

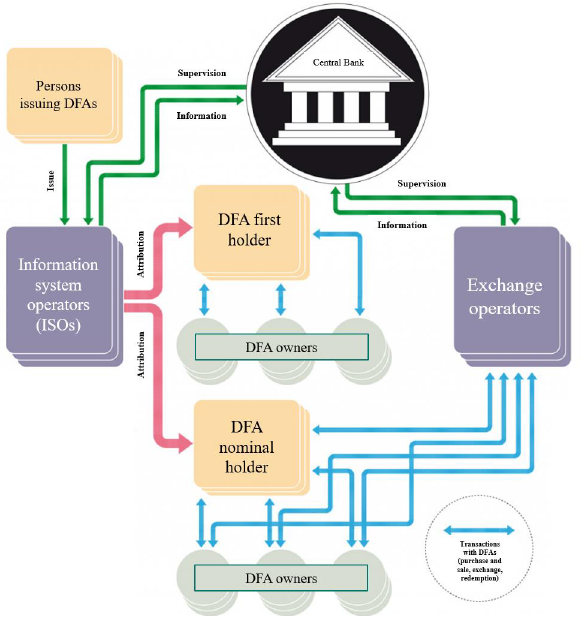

Let us consider in more detail the interaction of participants in the digital financial assets market in Fig. 2.

Рис. 1. Реестр операторов информационных систем, действующих в 2026 г.

Fig. 1. Register of information system operators (ISO) in 2026

Source: Bank of Russia, 2026.

Рис. 2. Схема взаимодействия участников рынка ЦФА

Fig. 2. Diagram of interaction between digital financial assets market participants

Source: [SmartLab]

Figure 2 suggests that the digital financial assets market comprises several key participants: issuers, information system operators, exchange operators, nominee holders, investors, and the Central Bank. Issuers issue digital financial assets through information system operators, who provide the technical infrastructure, digital asset accounting, and compliance with the rules for their issuance and circulation. After placement, the assets are transferred to their initial owners and can then be freely circulated among market participants.

The Central Bank plays a key coordinating and oversight role in the digital financial asset market. It regulates the activities of information system operators, sets requirements for the issuance and circulation of digital assets, and monitors compliance with current legislation. Exchange operators, in turn, facilitate digital asset purchase and sale transactions, while nominee holders are responsible for recording and maintaining ownership rights. Thus, the functioning of the digital financial asset market is based on a combination of blockchain technology infrastructure and government regulation mechanisms.

The Russian digital financial asset market has demonstrated steady growth over the past five years. According to SberCIB estimates, the total volume of digital financial asset issues in 2024 reached 455 billion rubles, including 649 unique issues, compared to only 35.2 billion rubles the year before. Comparable trends are reflected in the estimates provided by the Analytical Credit Rating Agency (ACRA). According to the agency, during the first eight months of 2024 the nominal value of digital financial assets in circulation increased nearly fourfold, rising from 60 to 217 billion rubles.

ACRA also reports that the cumulative volume of newly issued DFAs since the beginning of 2024, calculated on the basis of disclosed issuance amounts excluding repayments and amortization, reached approximately 182 billion rubles [ACRA, 2024]. At the same time, the assessment of the market remains complicated by the limited transparency of publicly available placement data, which makes it difficult to determine the overall market indicators with a high degree of accuracy.

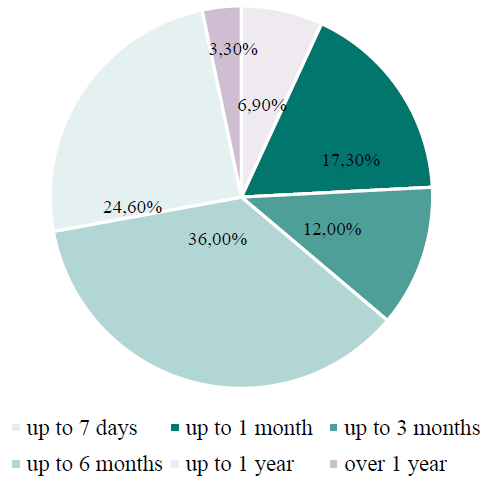

It is important to note that DFAs are mainly considered as a tool for attracting short-term investments (Figure 3).

Рис. 3. Периоды обращения ЦФА по выпускам в 2024 году

Fig. 3. DFA circulation periods by issue volumes in 2024

Источник: compiled by the authors based on [ACRA, 2024]

As Figure 3 shows, in 2024, less than 28% of all issuances were financial instruments with maturities longer than six months. The largest share (36%) were DFAs with maturities between three and six months. This is likely due to the fact that DFA issuers are still in the testing phase of issuance mechanisms, selecting the most effective scenarios for using the instrument, and simultaneously studying the structure and behavior of investors.

Now, the most widespread are simple forms of DFAs, that certifies monetary claims to the issuer. It is not surprising given the current stage of market development. In general, for most users, DFAs represent debt obligations, an analogue of classic bonds and instruments linked to the price of the underlying asset. The volume of debt DFAs is more than 431 billion rubles, and their volume in circulation is 207 billion rubles.

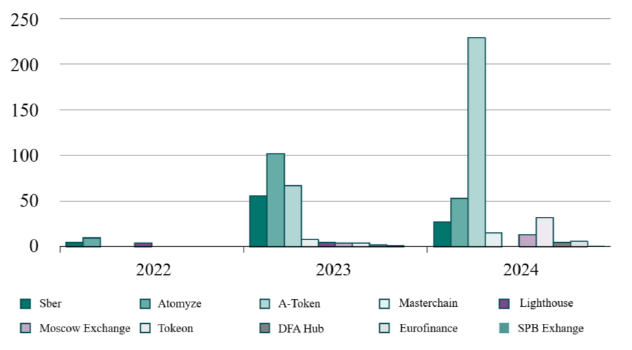

Fig. 4 shows the number of debt DFAs issued by various information system operators.

Рис. 4. Динамика выпуска долговых ЦФА операторами, аффилированными с Банком России (2022-2024 гг.)

Fig. 4. Dynamics of issuance of debt DFAs by operators affiliated with Bank of Russia (2022-2024)

Source: SberCIB, 2024a

According to Fig. 2, the most active DFA issuers are banks. Therefore, it is too early to discuss the development of the infrastructure in this market segment. However, the overall concentration of the DFA market remains very high. The two largest issuers, Alfa-Bank and VTB, account for 68 % of the total market volume (Fig. 3). In particular, out of 431 billion rubles of issued debt DFAs, 227 billion rubles (or 188 issues) were issued by Alfa-Bank on the A-token platform.

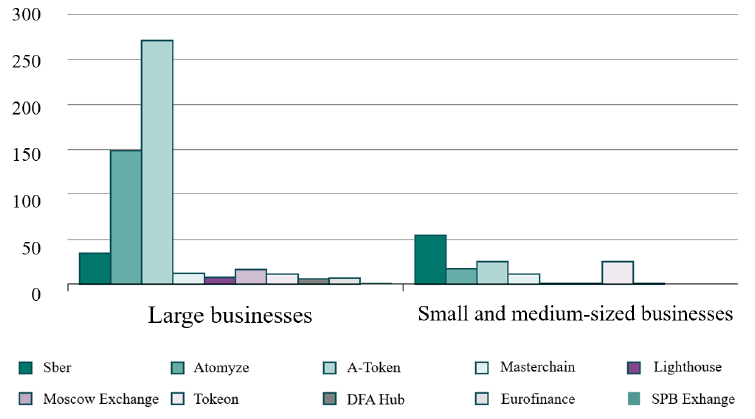

The number of unique corporate borrowers of DFAs has grown to 187. Analysis of the transaction structure shows that among the 187 issuers that have already tested the digital financial assets market, only 64 companies had previous experience in placing classic bonds (34 %). The number of borrowing companies has increased mainly due to the growth in the number of transactions in the small and medium-sized enterprises (SMEs) segment, where the greatest activity is observed on the Sber platform (Figure 5).

Рис. 5. Количество выпущенных ЦФА по платформам и типам эмитентов

Fig. 5. Number of issued DFAs by platforms and type of issuers

Source: SberCIB, 2024a

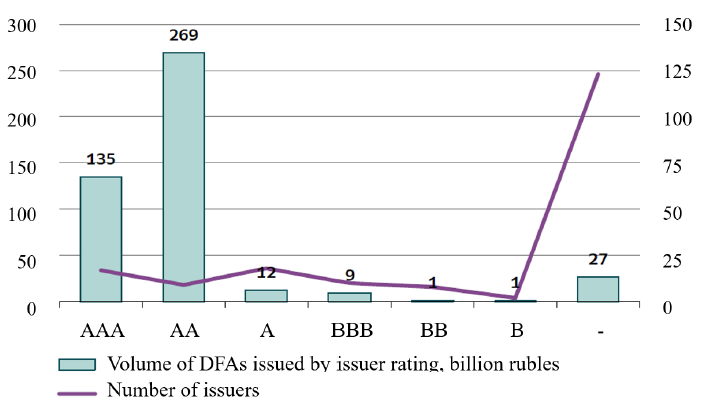

It should be noted that 125 companies that issued DFAs do not have a credit rating

or have a rating below “B”, the cumulative volume of their borrowings is 27.7 billion rubles or 193 issues (Fig. 6).

Рис. 6. Статистика ЦФА по рейтингам эмитентов

Fig. 6. Statistics of DFAs by issuer ratings

Source: SberCIB, 2024a

Market participants provide rather optimistic assessments regarding the future expansion of transaction volumes in the digital financial assets (DFA) sector. In particular, the Moscow Exchange estimates that the DFA market could reach 5-10 trillion rubles by 2027-2028. At the same time, more restrained projections also exist. For example, Expert RA forecasts market growth to approximately 500 billion rubles. Information system operators likewise expect substantial market expansion and predict that the DFA market may approach 1 trillion rubles within the next several years [Alfa-Bank, 2024].

Despite the high growth potential and rapid development of the sector, the DFA market still faces a number of significant constraints limiting its further expansion. One of the main challenges is the low level of activity in the secondary market, which largely remains confined to the platforms where the assets were initially issued. This contributes to market fragmentation and insufficient integration between operators.

Interaction between information systems is also complicated by the fact that operators rely on different blockchain infrastructures and business models. The Bank of Russia has already identified this issue as one of the regulator’s medium-term priorities [Bank of Russia, 2024a].

It is expected that the introduction of mechanisms for cross-selling DFAs between different platforms will partially address these limitations through exchange operators. In Russia, only the Moscow Exchange and the SPB Exchange currently have the required status to perform such functions. In addition, the DFA market participants expect the Russian Ministry of Finance to equalize the taxation of digital financial assets with the classical market in terms of combining tax bases. Today, non-credit institutions have a separate tax base for digital financial assets in a separate tax base, which is a negative factor for the issue of new assets.

Future market development is expected to be driven by the emergence of more sophisticated and customized digital financial products. This may become possible through the expansion of the range of underlying assets used for monetary claims within DFAs, as well as through an increase in the number of HDRs linked to art objects.

In 2025, the product line of digital financial assets (DFAs) expanded significantly, providing investors with new opportunities to diversify their investment portfolios. Specifically, DFAs linked to the value of cryptocurrencies such as Bitcoin and Ethereum emerged, as well as instruments focused on monetary policy parameters. The latter allow investors to formulate expectations regarding regulator decisions, including changes to the key rate, reflecting the deepening integration of digital instruments into the macroeconomic agenda.

At the same time, the segment of so-called "exotic" DFAs is developing, encompassing instruments with non-standard return mechanisms. These include assets linked to bank lending, venture capital investments, project financing, insurance events, and even charitable initiatives. The expansion of DFA functionality demonstrates market participants' desire to adapt this instrument to a wide range of financial needs, including risk hedging and alternative forms of capital raising [SberCIB, 2025].

The digital financial asset market for commodities has also seen significant growth, expanding beyond traditional metals to include instruments linked to oil, bitumen, cocoa, and wheat. This diversity of underlying assets allows investors to build portfolios with low correlation to traditional financial instruments, target specific market trends, and utilize additional risk management mechanisms.

Taxation of transactions with DFAs is regulated by the Russian Tax Code. According to Article 214.9 of the Russian Tax Code, the tax rate on income from digital financial assets transactions for individuals is 13% for residents and 30% for non-residents. Taxpayers are required to independently calculate and pay tax on income from digital financial assets transactions.

In recent years, Russia has seen some changes in the regulation of digital financial assets. Federal Law No. 325-FZ of July 14, 2022, amended Article 214.1 of the Russian Tax Code, clarifying the taxation procedure for income from transactions with derivative financial instruments whose underlying asset is a digital financial asset [Part Two of the Tax Code …].

One of the main problems in regulating digital financial assets is the lack of a clear distinction between different types of digital assets. Federal Law No. 259-FZ defines digital financial assets as digital rights, but in practice, difficulties arise in classifying assets, especially when it comes to hybrid instruments. For example, it is not always clear whether a specific token is a digital financial asset, a cryptocurrency, or a utility token [On Attracting Investments …]. This creates legal risks for issuers and investors, as different types of assets fall under different regulatory regimes. Furthermore, there are no clear mechanisms to protect investor rights in the event of bankruptcy of the issuer or exchange operator. Unlike traditional financial instruments, which have deposit insurance or compensation fund procedures, such mechanisms have not yet been developed for digital financial instruments.

The current regulatory system for digital financial instruments faces a paradox: strict licensing requirements for exchange operators are coupled with the need to stimulate innovation. High capital requirements for operators and complex licensing procedures create a situation where only large players can afford to enter the market, limiting competition and innovation.

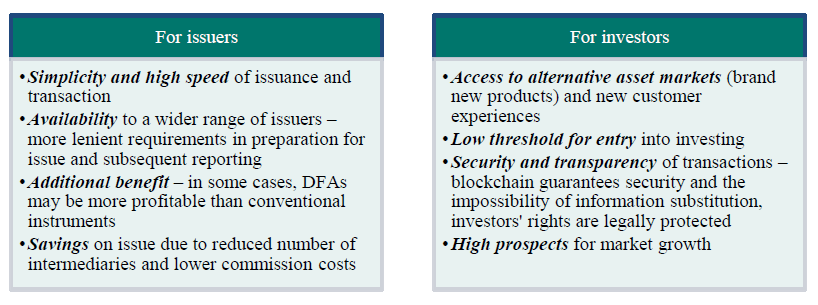

The structural and functional analysis made it possible to identify a number of features that increase the attractiveness of DFAs for financial market participants (Fig. 6).

Рис. 6. Преимущества ЦФА для участников финансового рынка в России

Fig. 6. Benefits of DFAs for financial market participants in Russia

Source: compiled by the authors

At the same time, one of the key limitations of this instrument remains the insufficient level of publicly available information, which complicates an objective assessment of the issuer’s creditworthiness. While short-term credit risks are generally assessed as moderate, in the case of long-term investments they may become significantly more substantial.

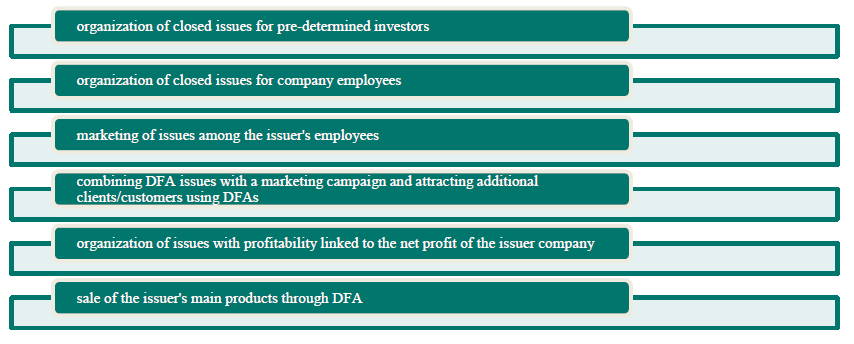

The study of the economic nature of DFAs also demonstrates that issuers may use these instruments not only to attract financing, but additionally as an effective mechanism for strengthening brand recognition and promoting the company in the financial market environment (Fig. 7).

Рис. 7. Создание новых возможностей для бизнеса с помощью ЦФА

Fig. 7. Creating new business opportunities through DFAs

Source: compiled by the authors

Conclusion

Digital financial assets represent a promising direction for the development of the Russian financial market. In this regard, further improvement of the institutional and regulatory framework remains highly important, including tax regulation, simplification of DFA circulation across different platforms, expansion of interaction between market participants, and broader opportunities for operators engaged in trading digital assets and utilitarian digital rights.

The analysis showed that DFAs are currently used mainly as an instrument for attracting short-term financing, while banks remain the dominant issuers in this segment. At the same time, the market infrastructure is still at an early stage of development, which creates a number of limitations, including low liquidity in the secondary market, insufficient integration between operators, and significant market fragmentation.

Despite these challenges, DFAs provide substantial advantages for both issuers and investors. For issuers, the main benefits include simplified issuance procedures, faster transactions, lower intermediary and commission costs, and more flexible requirements for asset placement. For investors, DFAs expand access to alternative investment instruments, lower entry barriers, and increase transaction transparency and security through blockchain technologies.

The study also demonstrates the significant potential of DFAs in cross-border settlements, particularly under sanctions-related restrictions and the growing importance of cooperation with friendly countries. The use of blockchain and smart contracts reduces dependence on intermediaries, accelerates transactions, and lowers operational costs. Asset tokenization therefore contributes not only to the development of new business models, but also to increased trade activity and broader economic growth.

Список литературы

С. 2675-2690.

С. 27-35. DOI: 10.21777/2587-554X-2024-1-27-35.

С. 75-130.

№ 3(704). С. 16-23.