Introduction

The Balanced Scorecard is defined as one of the solutions that allow companies to develop effectively and increase their income level [Bezmaternykh et al., 2022], which allows to be more competitive [Samán et al., 2022; Sousa et al., 2020] however, it is essential to carry out a more in-depth study of variables such as staff qualifications, company conditions and other internal and external variables that have an effect at the time of implementing this system [Bezmaternykh et al., 2022].

It is worth highlighting that to date, the academic community determines the balanced score as a factor of great importance and a notable factor in companies to date [Sousa et al., 2020; Suárez & Zaragoza, 2023] due to its characteristic in measuring processes in an individual and interactive way [Antonsen, 2014; Dudic et al., 2020] and in the diversity of its metrics [Banker et al., 2011] and impact on performance at the organizational level [Amado et al., 2012; Cardinaels & van Veen, 2010; Chen et al., 2011; Kaveh, 2019; Sousa et al., 2020], compromising the managers and productive units of an institution [Antonsen, 2014; Bezmaternykh et al., 2022; Suárez & Zaragoza, 2023].

In this sense, by using the BSC the company no longer needs inspectors since all personnel are trained and executing the process manual [Antonsen, 2014] as strategic measures [Banker et al., 2011; Bisbe & Barrubés, 2012]. However, there are studies that determine the difficulty of implementing the BSC [Banker et al., 2011; Ittner et al., 2003; Lipe & Salterio, 2000; Malina & Selto, 2001] at the same time the difficulties are mitigated using strategic mappings [Ittner et al., 2003; Santos et al., 2019]. The Balanced Score Card is essential for developing countries [Sousa et al., 2020], likewise it allows to identify advantages and disadvantages of the organization, allowing to search for possible solutions [Dudic et al., 2020], during the last three decades it is understood that the balanced score card is a tool that must be implemented in the organization for the effectiveness of the strategies [Atkinson, 2006; Tawse & Tabesh, 2023], because the tool is focused on learning through feedback, giving greater productivity to managers in decision making [Capelo & Días, 2009], as long as a reinforcement of the organizational culture has been implemented as a fundamental first step, so that the balanced

score card model does not fail [Deem, 2009].

In this virtue the objective of the research is to analyze Balanced Score Card and its impact on income in companies in the agricultural sector in zone 3 of Ecuador.

Materials and methods include a quantitative, correlational, mathematical- statistical, nonexperimental approach.

The companies in the agricultural sector of Zone Three of Ecuador were surveyed. According to the census and verification of secondary data found in the Superintendency of Companies, 60 companies were registered, which comply with the disclosure of profits for the year and the balance sheets on time before the regulatory body. Likewise, in addition to extracting the data in a documentary manner, field work was carried out using the complete inductive method and extracting the data through the application of a questionnaire, this to determine the use of the balanced score card within the companies. Once the database was available, the data of all the companies was organized in a descriptive manner in such a way that they could be aligned to a single dimension, in order to cross the dichotomous or nominal data with polytomous or ordinal data such as the Likert scale, thus arriving at a calculation of indices by obtaining the arithmetic mean, the variance and the standard deviation of all the data extraction items. After preparing the data, the descriptive tables were entered into the STATA software, which will support us in calculating the correlation of the variables through the linear regression of the income with reference to the balanced score card.

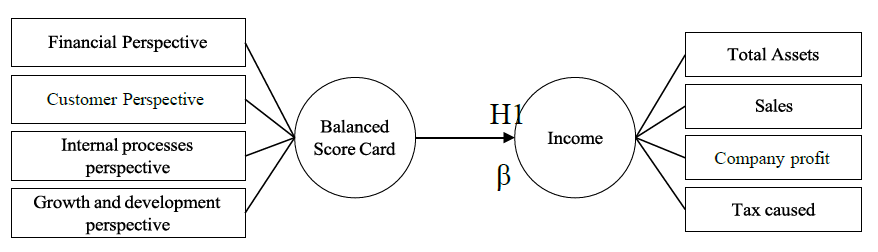

The research model is presented below in Figure 1.

Рис. 1. Исследовательская модель

Fig. 1. Research model

Once the theories of administration have been studied and the balanced scorecard has been reviewed, the qualitative hypothesis is defined, which will allow us to determine whether the two variables have a dependency relationship in the development of the economic growth of companies. H1: The balanced scorecard affects the economic and financial development of agricultural companies located in Ecuadorian territory.

Theoretical review

The balanced scorecard is a powerful tool for the entire organizational context. It also monitors the achievement of objectives through a traffic light system that allows the user to integrate the perspectives of learning and innovation, internal processes, customers and finance [Elbanna et al., 2022; Grigoroudis et al., 2012], It should be emphasized that not only can the balanced scorecard be used as an evaluator of the perspectives, but at the same time the evaluation of the supply chain is included [Bhagwat & Sharma, 2007; Bigliardi & Bottani, 2010; Shafiee et al., 2014].

The balanced score card model provides indicators on which it is based to measure the sustainability performance in the organization's systems [Fatima & Elbanna, 2023; Huang et al., 2014; Nicoletti et al., 2018; Pham & Vu, 2023; Rabbani et al., 2014; Wang et al., 2022], in the same way it is a tool that optimally proposes the evaluation and prioritization criteria of projects [Asosheh et al., 2010; Quezada et al., 2022], at the same time it is added that the model integrates the central systems of the organization such as resources, finances and production [Chand et al., 2005].

One of the perspectives on which it focuses in a significant way is the motivation of staff, for the development of their learning and the improvement of their performance within the productive processes of the company as the main axis for the fulfillment of the objectives [Kádárová et al., 2014; Santistevan et al., 2020; Viteri, 2015].

The tool itself guarantees continuous improvement of the quality of the service by

monitoring internal processes, providing continuous follow-up, to achieve objectives [Kaplan & Norton, 2005; Lazo et al., 2019; Mendes et al., 2012; Montoya & Bárbaro, 2011].

The balanced score card is not only based on the four organizational perspectives, but also adheres to one or more performance evaluation perspectives, but with a customer focus, that is, relevant information on the customer's needs and requirements is taken into consideration as an important input [Grande & Haynes, 2024; Kim et al., 2003].

The comprehensive business evaluation should not only be based on financial ratios, of course through them we can see the results of the year, but decisions should not be made only with the financial perspective, but with the comprehensive evaluation of the entire organizational system [Quintero & Fernández, 2017; Rivera et al., 2009].

It is necessary to design a balanced score card, with the financial perspective as a result of all the operationalization of costs and benefits, chart of accounts, liability management, financial efficiency and profitability of the year [Ghiglione, 2021; Payne & Talbott, 2007; Sánchez et al., 2016].

It is worth highlighting that the environmental perspective can be integrated into more than the four traditional ones, by adjusting gauges for the corporate ecological footprint, environmental education, waste analysis and fuel consumption in production [Espino et al., 2015].

Within the context of the balanced score card, electronic commerce is included, where the focus is business to business B2B, that is, the transfer of information between supplier- client businesses, thus being an evaluation of the operational capacity, the interrelation with the client, the level of growth of the internal client and the implemented financial processes, providing information in an agile manner from different sources that allow management to make decisions in an optimal manner [Chang & Graham, 2010; Liu & Du, 2008; Millones, 2012].

In addition to the traditional balanced scorecard, there are new approaches to new modalities of the tool, thus being a comprehensive resilience control panel, evaluating connectivity, risk and vulnerability, planning and response capacity [Ludin & Arbon, 2017; Molenda et al., 2023; Ramsey et al., 2020].

The application of the tool allows to overcome the primary vision of the economic in management, with the design of new indicators and perspectives, the flexibility of the model allows to adjust to different business systems [Carvajal et al., 2022; Gutiérrez et al., 2015].

The implementation of complementary strategies, with the balanced score card, results in achievable objectives, however, if the strategy is not aligned with the balanced scorecard, it will be of no use, wasting time and business resources [Bisbe & Barrubés, 2012; Braam & Nijssen, 2004; Lara & Manuel, 2017].

One of the fundamental parts of the balanced scorecard is the establishment of indicators, which reflect the dimension in terms of suitability, processes and competency tests [Méndez & Ordoñez, 2020; Salinas La Casta et al., 2009], analyzing the needs of the industry or company in which it is going to be sized [Neri et al., 2021; Valderrama et al., 2010].

The indicators that are mostly used are aimed at environmental control [Ahi & Searcy, 2015; Sosa, 2020].

Ultimately, and after the analysis of excellent authors who have contributed significantly to the topic of the balanced scorecard, it can be deduced that it is a holistic method, in which none of the perspectives should be left aside, those that are aligned with the strategy, for the achievement of objectives, thus making the balanced scorecard a fundamental tool for making decisions in a rational manner throughout the business system.

Business revenues are of vital importance for their survival and competitiveness [Castillo & Villalba, 2018; Govea et al., 2012; Guerrero & Escorcia, 2011].

Administrative tools and their cost analysis result in a comfortable and accessible price for customers, thus demonstrating their loyalty and future business growth [Barragan Roncal et al., 2020; Merchán Martínez, 2018; Olmos Martines, 2023].

Sales increase when internal processes are analyzed and strategically changed to benefit all production units [Baque Villanueva et al., 2022; Caballero & Lara, 2021; García & Orland, 2011].

The implementation of accounting software has a positive impact on the analysis and improvement of company profits [Burgos Obeso & Suarez Cruz, 2017; Mendizábal Fernández, 2019; Valencia, 2019].

The balanced score card is based on different theories, where the study and the epistemology of terms that complement the study are clearly defined, thus giving a greater understanding of the applicability, development, functionality and the result obtained from the different studies carried out by authors of great relevance in the subject of decision-making based on the management tool.

The General Systems Theory founded by biologist Ludwig von Bertalanffy, states that all systems, regardless of their disciplinary domain, share some important similarities in their underlying structure [Bertoglio, 1982; Quiroz et al., 2021; Ríos & Santillán, 2016].

According to the theory of organization, the life of people in society depends on organizations, and these depend on the work of people [Sánchez, 2023; Tovar, 2009].

The general theory of administration is very pronounced by different authors, thus finding a tool that is used in all the activities of routine life and that once understood and applied in organizations, the objectives planned in advance can be conceived [Chiavenato, 2019; Fayol, 1916; Hernández, 2014; Koontz et al., 1991].

The theories support the formulation of the balanced scorecard, always seeking to achieve objectives, but at the same time maintaining control of all the productive units of an organization that can be managed in the first place by the four perspectives, that of staff development, internal processes, the client and the financial area and in the second place other perspectives can be added according to the needs of each of the functions that the company manages.

Econometric model: the econometric model was based on the simple linear regression formula represented in formula 1:

𝑦 = 𝛽0 + 𝛽1 ∗ 𝑋 + 𝜀 (1)

Where:

y= variable to be predicted;

X= variable that causes the change in variable “y”

β0= intercept

β1= coefficient associated with the variable of interest

ε= error

From formula 1 we obtain formula 2

𝐼𝑛𝑐𝑜𝑚𝑒𝑠 = 𝛽0 + 𝛽1 ∗ 𝐵𝑎𝑙𝑎𝑛𝑐𝑒𝑑 𝑆𝑐𝑜𝑟𝑒 𝐶𝑎𝑟𝑑 + 𝜀 (2)

Where:

β0= is the ordinate at the origin; β1= the slope coefficient;

ε= error.

Subsequently, the variables were standardized and Cronbach's alpha was calculated.

The validity of the Balance Score Card variable instrument was verified using Cronbach's Alpha with a score of 0.7634 and for the Income variable instrument it was 0.7455. These results are within the ranges demonstrating the validity and reliability of the instruments.

With the results of the standardized observations, indices were obtained using multivariate Principal Components analysis.

Research Results and Discussion

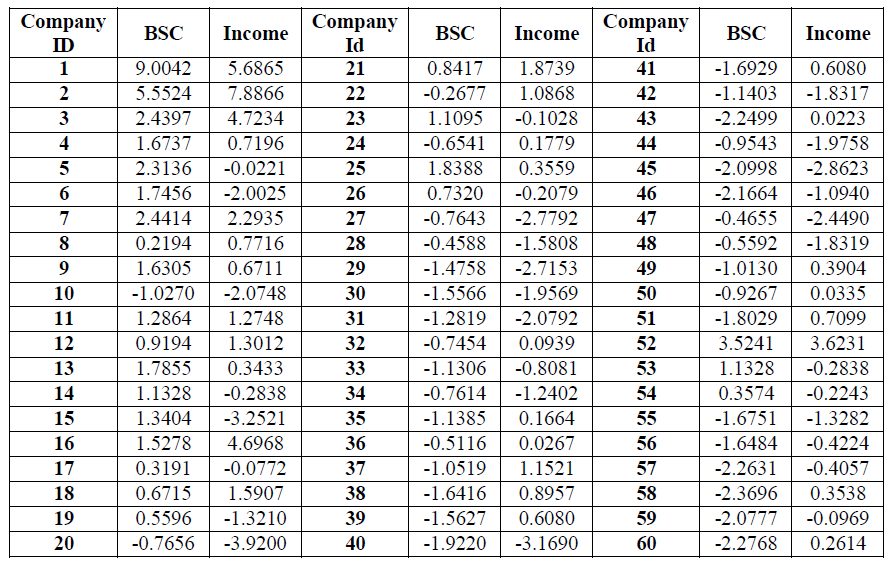

Таблица 1

Создание индекса между сбалансированной системой показателей и доходом

Table 1

Index creation between Balanced Scorecard and Incomes

From Table 1, it is interpreted that BSC values vary considerably across companies, from

-2.3696 to 9.0042. This suggests that some companies have superior performance in their BSC metrics, which could correlate with better revenues.

Companies with High BSC: For example, Company 1 has a BSC of 9.0042 and revenue of 5.6865, indicating positive performance in both metrics.

Companies with Low BSC: In contrast, company 60 has a BSC of -2.2768 and revenues of 0.2614, suggesting poor performance on the BSC and moderate revenue. It is observed that

companies with higher BSC values tend to have higher revenues.

Successful Companies: Those with a positive BSC (e.g., companies 1, 52, and 2) appear to have relatively high revenues, suggesting that BSC implementation may be contributing to their financial success.

Poorly Performing Companies: Companies with negative BSCs (such as companies 45, 46, and 57) tend to report low or negative revenues, indicating that poor BSC management may be limiting their ability to generate revenue.

Hypothesis testing

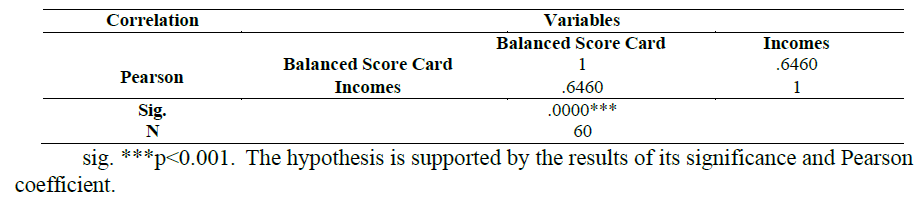

Таблица 2

Корреляция Пирсона

Table 2

Pearson correlation

Table 2 shows a positive average correlation of .6460, which determines that the variables are dependent and directly

proportional, meaning that when the BSC rises or increases income, they do so in the same way.

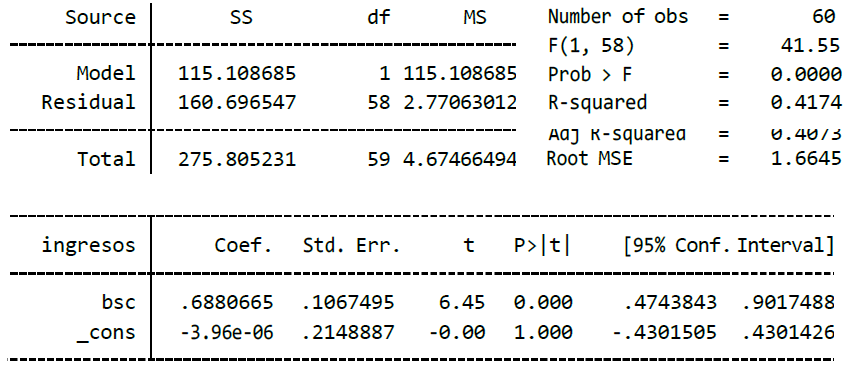

Таблица 3

Линейный регрессионный анализ

Table 3

Linear regression analysis

From Table 3, the following results were obtained:

The Balanced Scorecard explains 41.74% of the variability in revenue, which means that 58.25% of the revenues of the companies in the agricultural sector are in a different type of context.

For every unit that increases in the Balanced Scorecard, the revenue increases by

0.68 units, and this is statistically significant with 95% confidence p = 0.000, < 0.05, which means that the data was not analyzed randomly.

When the Balanced Scorecard is 0, the company's revenue will be 0.00006.

Intercept (β0): The slope of 0.68 implies that for every additional unit in the BSC, an increase of 0.68 in revenue is expected. This finding is statistically significant (p=0.000), suggesting that the observed relationship is robust and not due to chance. This result highlights that effective BSC management can translate into a tangible increase in revenue, underlining the importance of adopting strategies that optimize performance in this area.

Slope (β1): The coefficient is 0.68, which implies that for every unit of increase in the BSC, revenue increases by 0.68 units. This result is statistically significant (p=0.000), indicating that the observed relationship is robust and not the result of chance. This reinforces the idea that better management and performance on the BSC is associated with higher revenue.

Linear regression demonstrates a positive and significant relationship between the Balanced Scorecard and revenues in the agricultural sector. The results suggest that effective BSC implementation can be an important predictor of financial performance. However, it is crucial to consider other factors that may be affecting revenues and that have not been included in this analysis. Future studies could explore these additional variables to provide a more complete picture of the determinants of financial success in this sector.

Conclusion

The analysis reveals a positive average correlation of 0.6460 between the Balanced Scorecard (BSC) and revenues, indicating that both variables are dependent and directly proportional. This finding suggests that an increase in the BSC is accompanied by an increase in the revenues of companies in the agricultural sector.

In addition, An R2 of 41.74% indicates that the model is able to explain less than half of the variability in revenues. This suggests that, although the BSC has a considerable impact, there are other factors that influence revenues, accounting for 58.25% of the unexplained variability. This aspect emphasizes the need to consider a more holistic approach that includes other relevant variables in the analysis of financial performance.

It has been found that, for each unit of increase in the BSC, revenues increase by 0.68 units, with a robust statistical significance (p=0.000), which reinforces the validity of the data analyzed and suggests that the results are not a product of chance. Even when the BSC is set to zero, it is estimated that the companies' revenues would have a minimum value of 0.00006, indicating that the BSC has a tangible impact on financial performance.

The significant correlation of 0.64 between BSC and revenue supports the acceptance of Hypothesis 1: BSC benefits the revenue of companies in the agricultural sector. Through the creation of indices using principal components, patterns have been identified that suggest that management aligned with the BSC is associated with better financial performance.

Consequently, companies in the agricultural sector are recommended to carry out a thorough evaluation of their strategies and practices in relation to the BSC. Training and the alignment of their organizational objectives with BSC metrics are essential to boost both performance and revenue. Future studies should delve deeper into the application of additional statistical methods to validate these observations and provide a more robust framework for strategic decision- making.

Practical Implications

Improving Financial Performance: Companies in the agricultural sector can benefit from implementing the Balanced Scorecard as a strategic management tool. By focusing on key metrics, organizations can identify areas for improvement that potentially increase their revenues.

Training and Development: It is essential to invest in training for staff in the use and understanding of the BSC. This will ensure that all levels of the organization are aligned with strategic objectives, which can translate into better overall performance.

Strategic Alignment: Companies should review and adjust their strategies to align with the BSC metrics. This may include redefining objectives and implementing practices that reinforce the focus on financial results.

Continuous Monitoring and Evaluation: Implementing a regular monitoring system for BSC metrics will allow companies to make proactive adjustments to their strategies, ensuring continuous improvement in their performance.

Theoretical Implications

Validation of the BSC as a Management Tool: The results of the study reinforce the theory that the BSC is an effective framework for managing organizational performance, especially in agricultural contexts. This theoretical validation may encourage future studies on its applicability in different sectors. Relationship between Non-Financial Indicators and Financial Performance: This article contributes to the existing literature on how non-financial indicators (such as those of the BSC) can influence and predict financial results. The door is opened to additional research exploring this relationship in other

contexts.

Development of New Theoretical Models: The findings suggest the need to

develop theoretical models that integrate the BSC with other contextual factors that affect revenues. This could enrich the existing conceptual framework and provide a deeper understanding of the dynamics of organizational performance.

Future Research: The need for longitudinal studies assessing the impact of the BSC over time is raised, as well as research examining other sectors, which could expand the applicability of the findings and theories proposed in this article.

Reference lists