РАЗВИТИЕ МЕТОДИЧЕСКИХ ПОДХОДОВ К МИНИМИЗАЦИИ БАНКОВСКИХ РИСКОВ В СИСТЕМЕ МОНИТОРИНГА И ПРОГНОЗИРОВАНИЯ

Aннотация

В статье обобщены основные методы и инструменты системы риск-менеджмента и выделены основные этапы мониторинга банковских рисков, на основании чего произведено построение организационного механизма функционирования информационно-аналитической системы мониторинга банковских рисков с учетом развития цифровых технологий и возникновения сопутствующих им цифровых рисков. Данная система представляет особой многофункциональный комплекс показателей исследования внешней и внутренней финансовой среды банка.

Разработана комплексная вариантная система сценарного прогнозирования банковских рисков, в контексте сценарных прогнозов в системе рассмотрены оптимистичный, рецессивный и пессимистичный прогнозы. В качестве метода раннего предупреждения банковских рисков в краткосрочной и среднесрочной перспективе предлагается стресс-тестирование. Даны рекомендации по организации процедуры стресс-тестирования и выделены конкретные этапы применения сценария стресс-тестирования в исследовании банковских рисков с учетом цифровизации банковских услуг.

К сожалению, текст статьи доступен только на Английском

Introduction

In banking, risk management is one of the key areas along with business, since competent risk management has a direct impact on the efficiency of commercial bank operations. The rapid pace of digital transformation across the world and the strong adoption of digital banking are changing the ways in which banks have traditionally provided financial services, which in turn entails the emergence of new problems and risks associated with digitalization. The main problems that arise during the transition of the banking system to digital technology include such things as a lag in regulation, an increase in the number of cyberattacks during various operations, and the complication of management systems for various processes in the mechanism of digital technology [Vaganova O.V., Melnikova N.S., Dikareva E.V., Kovaleva A.P., Lavrina A.O., 2023]. Today, digital risks are a young branch of banking risk management, but they require the development and application of specific tools to minimize them. Under the current conditions, a high-quality system for monitoring and forecasting banking risks is needed, taking into account the development of digital technology.

Objective. The purpose of this study is to develop methodological approaches to minimize banking risks in the monitoring and forecasting system, taking into account the introduction of digital technology into banking activities.

Methods. This study is based on the principles of system and structural approaches. The study has been conducted using materials of scientific works of foreign and Russian scientists and economists in the field of banking, which allowed to generalize existing concepts and approaches for developing a comprehensive variant system of three-scenario forecasting of banking risks based on stress testing. The objective has been achieved by means of generalization and comparison, analysis and synthesis, grouping and various illustrative techniques.

Results and Discussion

The introduction of digital banking technology brings both a certain list of benefits to clients and exacerbates a number of risks that commercial banks need to address and respond to in order to reduce their impact [Vaganova O.V., Talimova L.A., Gordya D.V., 2023]. The key task of risk management is to maintain acceptable ratios of profitability with security and liquidity indicators in the process of managing commercial bank assets and liabilities, that is, minimizing bank losses.

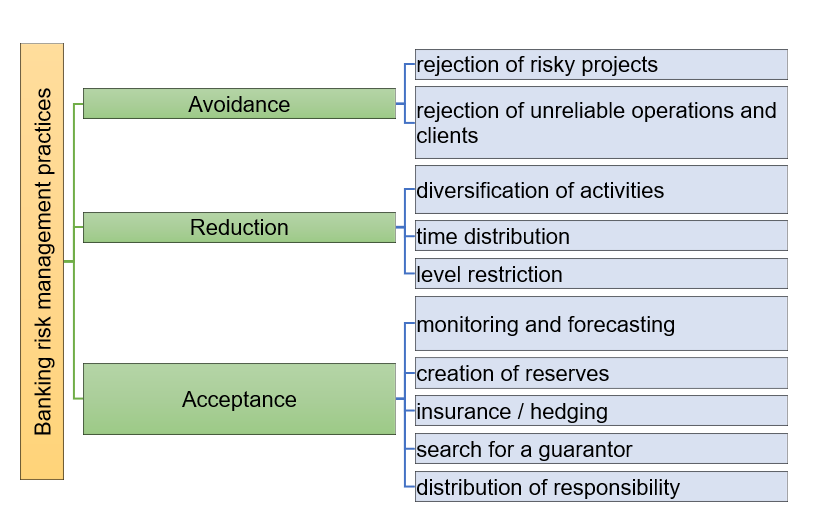

In practice, banks use a system of measures to reduce risk to the minimum possible level using the following groups of risk management methods, presented in Fig. 1.

Рис. 1. Основные методы и инструменты системы управления банковскими рисками

Fig. 1. Main methods and tools of the banking risk management system

It is important to note that banking in Russia is characterized not by avoiding risk altogether, but by anticipating, monitoring and reducing it to an optimal level. The correct organization of work of commercial bank units requires full and multi-stage analytical work [Skaldina L.S., 2020]. By assessing threats, analyzing potential risk impact, evaluating existing controls, developing and implementing a risk mitigation plan, and regularly monitoring and analyzing the effectiveness of the plan, commercial banks can minimize cyber-attack risks, financial losses, reputational damage, legal and regulatory consequences, and operational disruptions [Amsaveni N., Dharshini M., Evangeline H., 2023].

The essential characteristics of monitoring banking risks are multifaceted; they can be grouped according to forms

of control, information and analytical systems, integrative-indicative diagnostic systems

of risk status.

The presented characteristic features of banking risks “are based on the interpreted parameters of the diagnosed risk and allow identifying, analyzing, evaluating, and monitoring each risk separately and the totality of risks in the overall risk management system of a commercial bank” [Comprehensive insurance …]. We present the main stages of the monitoring process in Table 1.

Таблица 1

Основные этапы процесса мониторинга банковских рисков

Table 1

Main steps of the banking risk monitoring process

Step name | Step characteristics | Result |

Exchange of information and consultation | - developing a plan for the exchange and use of information; - defining the scope of risk management; - studying and analyzing cause-and-effect relationships; - selecting methodological approaches for risk identification and analysis; - analyzing different opinions in risk assessment; - ensuring appropriate risk identification; - ensuring approval and support for the risk treatment plan | Stakeholders facilitate the exchange of information about the risk management process with other elements of the system, such as managing macroeconomic changes, developing programs for collecting, processing and using the necessary information and its exchange |

Establishing the scope of risk management | - defining the main parameters, scope and criteria of the risk analysis process; - defining and coordinating the objectives of risk assessment, risk criteria and risk assessment program; - defining the external and internal environment of the bank, the objectives of risk management activities, as well as classification of hazardous events | The step allows to determine the main management parameters, scope of application and criteria of the risk management process of banking activities taking into account the market situation, macroeconomic dynamics, structural changes, development of infrastructure and client base |

Risk analysis and assessment | - the need to undertake appropriate methods and tools, absolute and relative assessment criteria; - methods of maximum influence on the bank’s activities, implementation of risk reduction opportunities; - the need to process risks, their grouping; - the choice between different types of risk - the priority of risk processing actions; assessment of the risk processing strategy that allows reducing the risk to an acceptable level | Risk assessment provides an understanding of possible hazardous events, their causes and consequences, the likelihood of their occurrence and the adoption of correct management decisions |

Risk treatment | - making and implementing one or more risk treatment decisions that allow changing the probability of a hazardous event and/or its impact; - identifying the conditions for formation and stages, trend dependencies and risk size | Risk treatment is an adaptive process of testing a risk for its acceptability and compliance with previously established criteria to determine the need for further risk treatment, monitoring and forecasting |

Risk forecasting | Conducting an audit regarding: - the reliability of the assumptions on which the risk assessment is based, including external and internal factors, parameters, static and dynamic indicators; - the compliance of the risk assessment results with actual risk information; - the correctness of the application of methods for identifying, analyzing, assessing and managing banking risks; - risk processing, monitoring and forecasting | Risk monitoring and forecasting are an integral part of the risk management process and are recorded in the report |

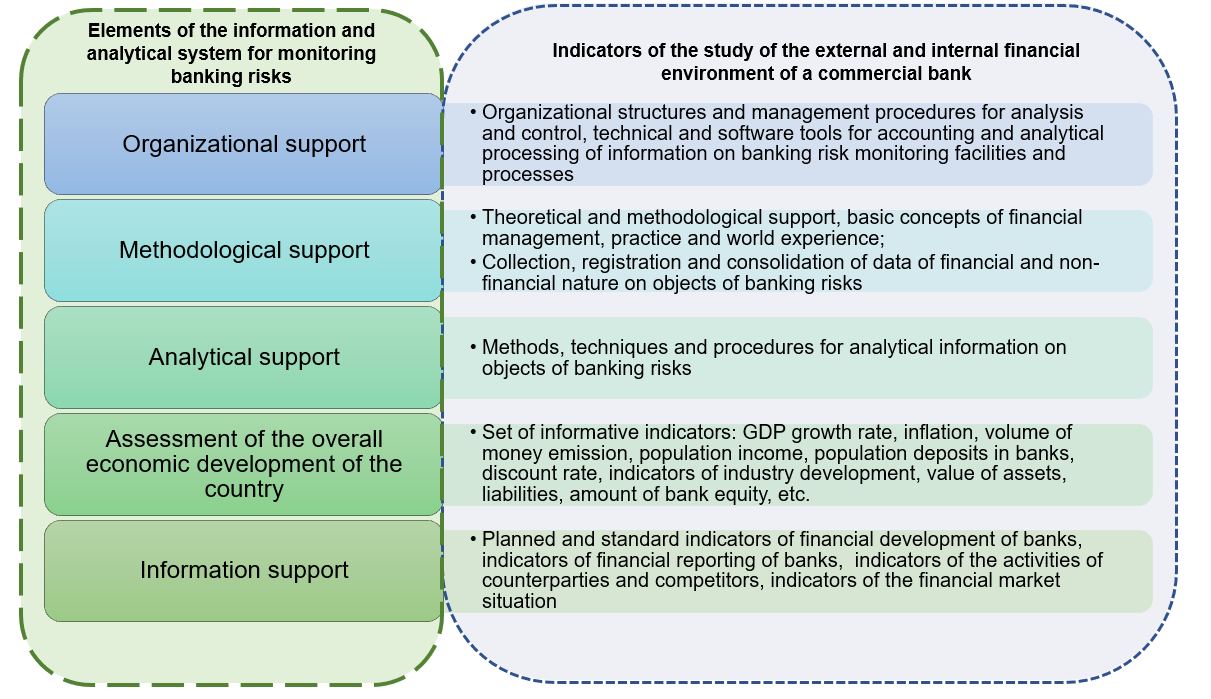

The main principles of building an intra-bank risk management system include complexity, differentiation, a single information base and coordination of management of different types of risks [Kara D.A., 2023]. For a more in-depth implementation of the monitoring and forecasting process, it makes sense to develop an organizational mechanism for the functioning of the information and analytical system in order to make adequate decisions on monitoring and forecasting banking risks (Fig. 2).

Рис. 2. Организационный механизм функционирования информационно-аналитической системы мониторинга банковских рисков

Fig. 2. Organizational mechanism for the operation of the information and analytical system

for monitoring banking risks

Thus, the analytical information system includes a list of indicators that are most relevant for monitoring, forecasting and management of the banking system and presents a special multifunctional set of indicators for studying the external and internal financial environment of the bank. The content of the information and analytical system is determined by numerous factors, among which the scope of the bank’s activities, the organizational and legal form of its functioning, as well as specific features of development in conditions of economic and political instability.

The identification of the main stages of the process of monitoring banking risks and the generalization of elements of the information and analytical monitoring system for minimizing banking risks that have arisen as a result of the digital transformation of the economy suggests proposing stress testing as a method of early warning of banking risks in the short and medium term [Gordya D.V., 2023].

The calculation of the predicted risk level for each component of the balance sheet should be carried out on the basis of a comprehensive stress-testing system, based on a “top-down analysis”.

The formation of the current capital requirement is a dynamic process that is carried out on a monthly basis, adjusting, among other things, the predicted capital value. For this purpose, regulatory and economic capital are calculated at the bank level. Regulatory capital is calculated based on the requirements of the Basel Committee; economic capital is calculated based on an internal assessment of all banking risks, as well as new risks of digitalization of services. As part of monitoring the adequacy of economic capital, a commercial bank develops several target scenarios for stress testing (both developed by regulatory authorities and internal specific scenarios), which are aimed at checking the stability of capital and its capabilities under various shock deviations.

It is assumed that the procedures related to risk management are implemented in the bank’s activities in such a way that the assessment of sensitivity to external and internal changes is carried out for all items of the bank’s financial position report [Dawodu S.O., Omotosho A., Akindote O.J., Adegbite A.O., Ewuga S.K., 2023]. In addition to checking the sensitivity of the components of banking risks, it is necessary to carry out procedures to assess the sensitivity of the coefficient (level) of return on capital in various shock situations.

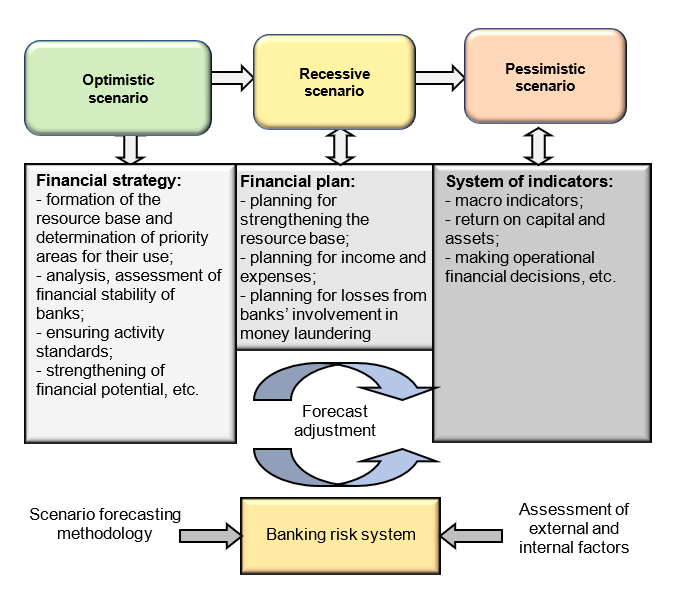

Sensitivity to such factors as political, economic and social conditions is assessed. These factors are considered from the position of increasing the impact on risks, actual or predicted situations, on the basis of which stress testing of the stability and reliability of banking activities is carried out. These factors are adjusted for the basic factor of capital adequacy. These procedures ensure that the bank is aware of all potential and existing risks to which it is exposed, since its components are being modified in accordance with the risk management strategy. Fig. 3 presents a comprehensive system of scenario forecasting of banking risks.

Рис. 3. Комплексная система сценарного прогнозирования банковских рисков

Fig. 3. Comprehensive system of scenario forecasting of banking risks

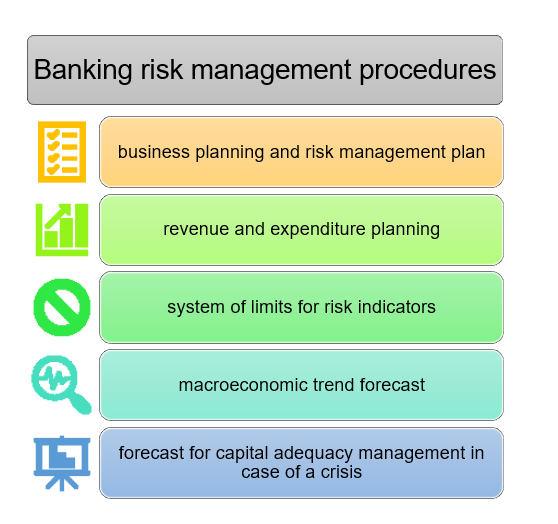

In the context of the scenario forecasts, we will consider the optimistic, recessionary and pessimistic forecasts, which represent a set of financial and economic relations, quantitative and qualitative indicators, taking into account the bank’s digital risks [Bochkareva E.V., 2023]. Planning the level of exposure to digitalization risks should be carried out annually, however, the forecast can be adjusted taking into account the current economic situation in the country and in the world. The process of managing banking risks should be carried out on a centralized basis and through the following procedures, presented in Fig. 4.

Рис. 4. Процедуры управления банковскими рисками

Fig. 4. Banking risk management procedures

We recommend the following approaches to stress testing:

a) top-down, i.e. assessing the impact of scenarios through analysis of the sensitivity of bank assets and liabilities to risks arising from digital technology;

b) bottom-up, i.e. assessment of the impact of individual risks (digitization criteria) on the bank’s economic capital.

In particular, with regard to return on capital, stress testing is carried out from the position of checking the possibility of maintaining the required level of capital under stress conditions. In this case, we propose to adopt the following as the main indicators of digitalization: “Communications”, “Payment services and technology”, “Product design”. Requirements for scenarios include plausibility, significance (minimum loss of 0.1 %) and simplicity.

The two-sided approach of foreign banks to capital assessment is assessing from the stress test position of adequacy of absolute value of own funds and from the stress test position of quantitative value of risks. This approach provides a complete picture of the commercial bank’s equity. Thus, the quantitative analysis of risks allows to calculate a minimum acceptable capital value of the bank that will allow to offset these risks.

The scheme for conducting the stress testing procedure for banks in relation to resilience to the risks of digitalization of services should take into account the tasks that stress testing solves, namely determining the bank’s resilience to changes in external factors and identifying new external factors that affect the level of risk [Kujur T., Shah M.A., 2015].

Historical analysis of variability of factors affecting the level of risk should be used. Corrective actions in stressful situations are an integral part of the scenario forecasting.

The frequency of stress testing is an important element of the procedure. In case of significant fluctuations in the economy, the scenario methodology can be complemented by developing potentially new sources of capital base increase, which will lead to better banks’ resilience.

Additional stress testing of absolute indicator allows assessing the ability of the actual capital to respond to changes due to digitalization of services, including changes in banking risks. As a result of developing the stress testing procedure, it is advisable to designate all the parameters and stages of the procedure from the standpoint of international requirements and the requirements of the domestic legislation of the country.

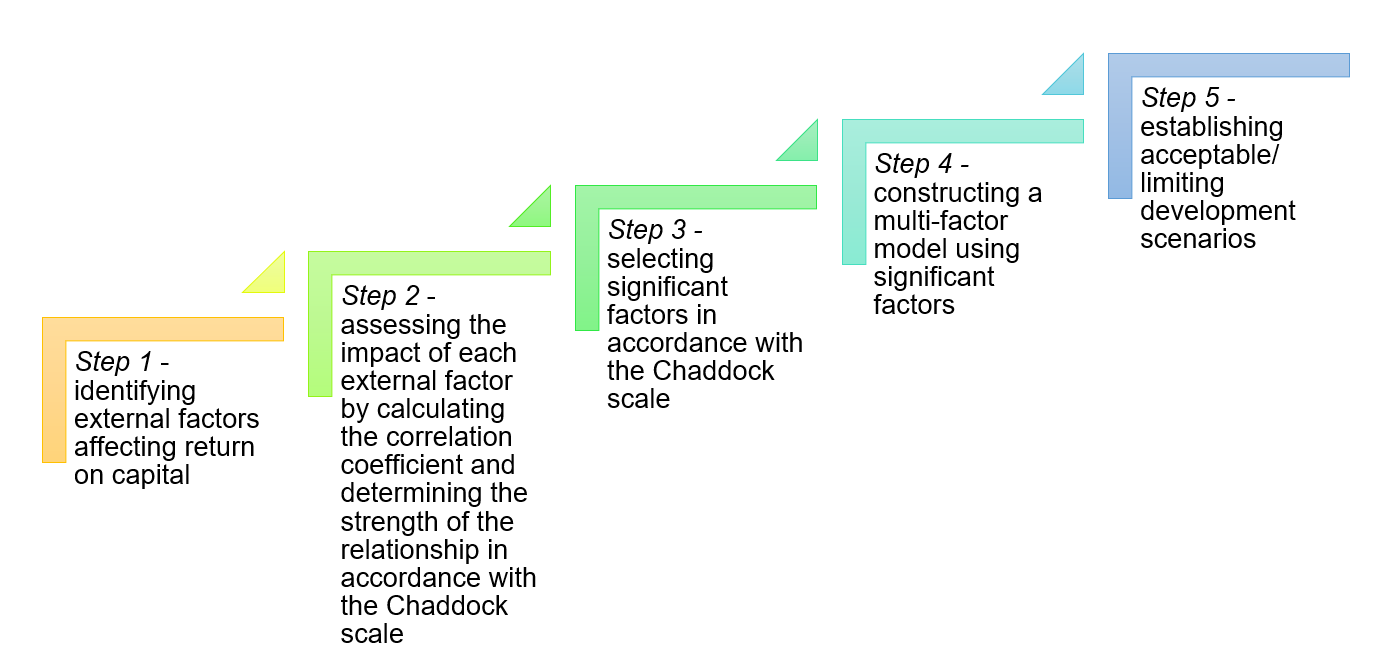

In the future, for the development of stress testing procedures in the study of banking risks, we consider it appropriate to use indicators characterizing the degree of interrelation, according to the Chaddock scale [Chaddock scale], which determines the closeness of the relationship as follows: 0 means complete absence of correlation; 0-0.3 is very weak; 0.3-0.5 is weak; 0.5-0.7 is average; 0.7-0.9 is high; 0.9-1 is very high. Step-by-step algorithm for actions to identify factors involved in stress testing is shown in Fig. 5.

Рис. 5. Этапы применения сценария стресс-тестирования в исследовании банковских рисков

Fig. 5. Steps of the stress-test scenario in banking risk studies

Conclusion

Based on the above, it is worth noting that the development and implementation of a new method for forecasting the impact of the level of digitalization of services on banking risks, which forms the basis of the monitoring methodology, make it possible to integrate additional parameters into the current system of indicators for assessing banking risks. These parameters are the degree of influence of digitalization and possible limits of deviations from the actual values of the bank’s financial stability. Such an addition to the system of indicators for assessing banking risks will make it possible to more effectively perform control functions in the future and will serve as a methodological tool for strategic planning of the activities of an individual commercial bank at the macro level. The use of predictive methods for early warning of deviations in economic indicators will allow identifying such situations and taking timely measures to eliminate undesirable consequences.

Список литературы

С. 912-916.

О.В. Вагановой, Н.Е. Соловьевой. Белгород: ИД «БелГУ» НИУ «БелГУ», 2023.С. 14-19.

Pp. 207-212.